ESRS Is No Longer Mandatory — What Should Your Business Do Next?

For many businesses, the Omnibus package came as a surprise. Companies that had already begun their sustainability reporting journey — investing in data collection, hiring consultants, allocating budget — suddenly found themselves exempt from the ESRS requirements. Some paused their efforts. Others cancelled them altogether. But a notable few pressed on voluntarily, recognising that the value of sustainability reporting extends beyond regulatory compliance.

Understanding where your business sits within the current regulatory landscape is the first step toward making informed decisions — both for the short and long term.

A Shifting Regulatory Landscape

The ‘simplified’ ESRS was developed to make sustainability reporting more accessible to companies. But easier does not mean straightforward — particularly for companies now sitting in the grey zone created by the Omnibus exemptions.

These companies are technically classified as large enterprises, yet are no longer required to report under the ESRS. They fall into a gap: too large for the voluntary standard designed for SMEs, but no longer bound by the directive intended for large companies. The result is a kind of regulatory limbo.

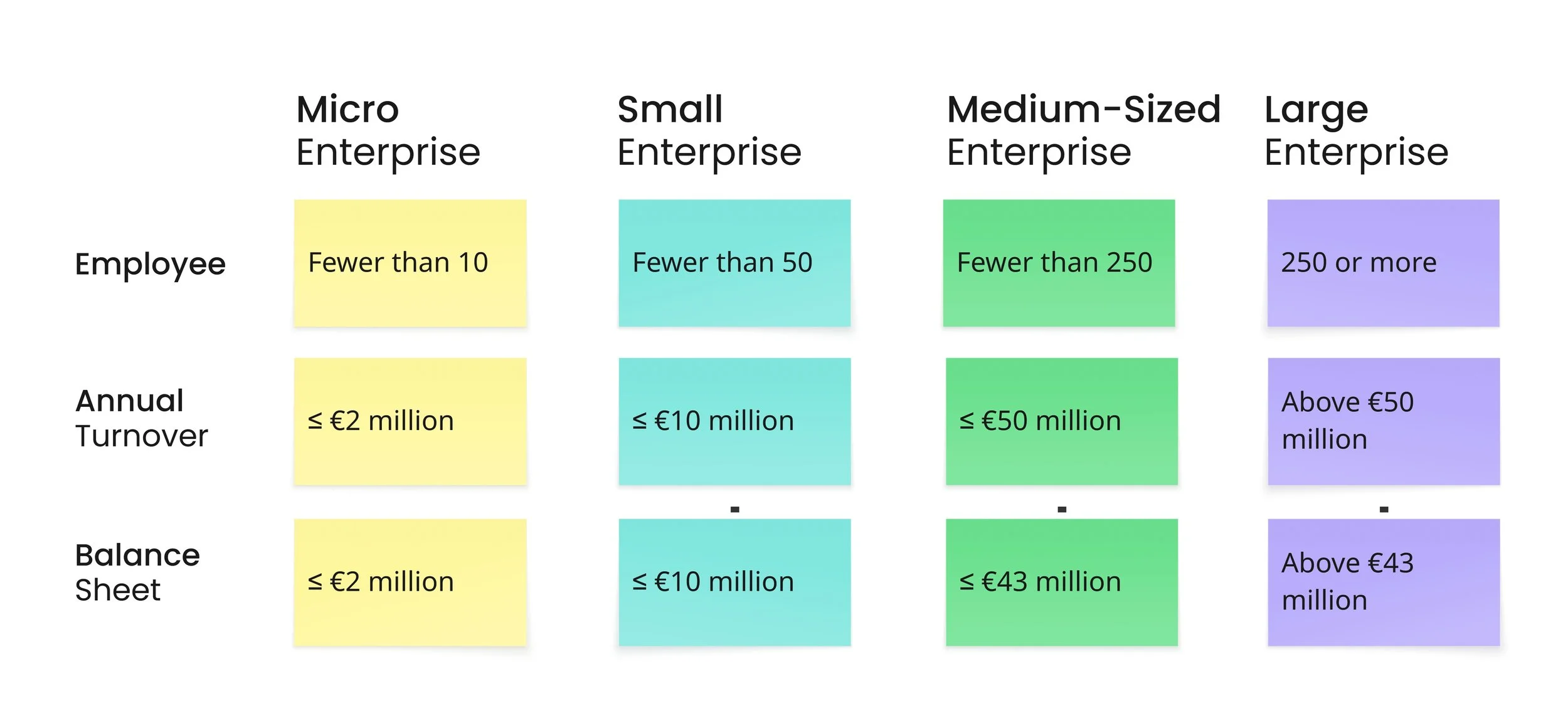

Types of companies in Europe

During the EFRAG SME Forum meeting on 6 February 2025, this question was raised directly. While no definitive answer was provided, one possibility discussed was that the VSME — the voluntary standard developed for small and medium-sized enterprises — could be renamed and extended to accommodate companies currently in the exemption category. Another possibility, though unlikely given current global volatility, is that the simplification process could result in exemptions being removed entirely, bringing these companies back within scope.

In the meantime, companies in this position are responding in three ways: some are continuing sustainability reporting efforts voluntarily; some are pivoting to alternative frameworks such as EcoVadis, ISO sustainability standards, or B Corporation certification; and others are stepping back from external reporting altogether, redirecting energy toward improving internal sustainability practices.

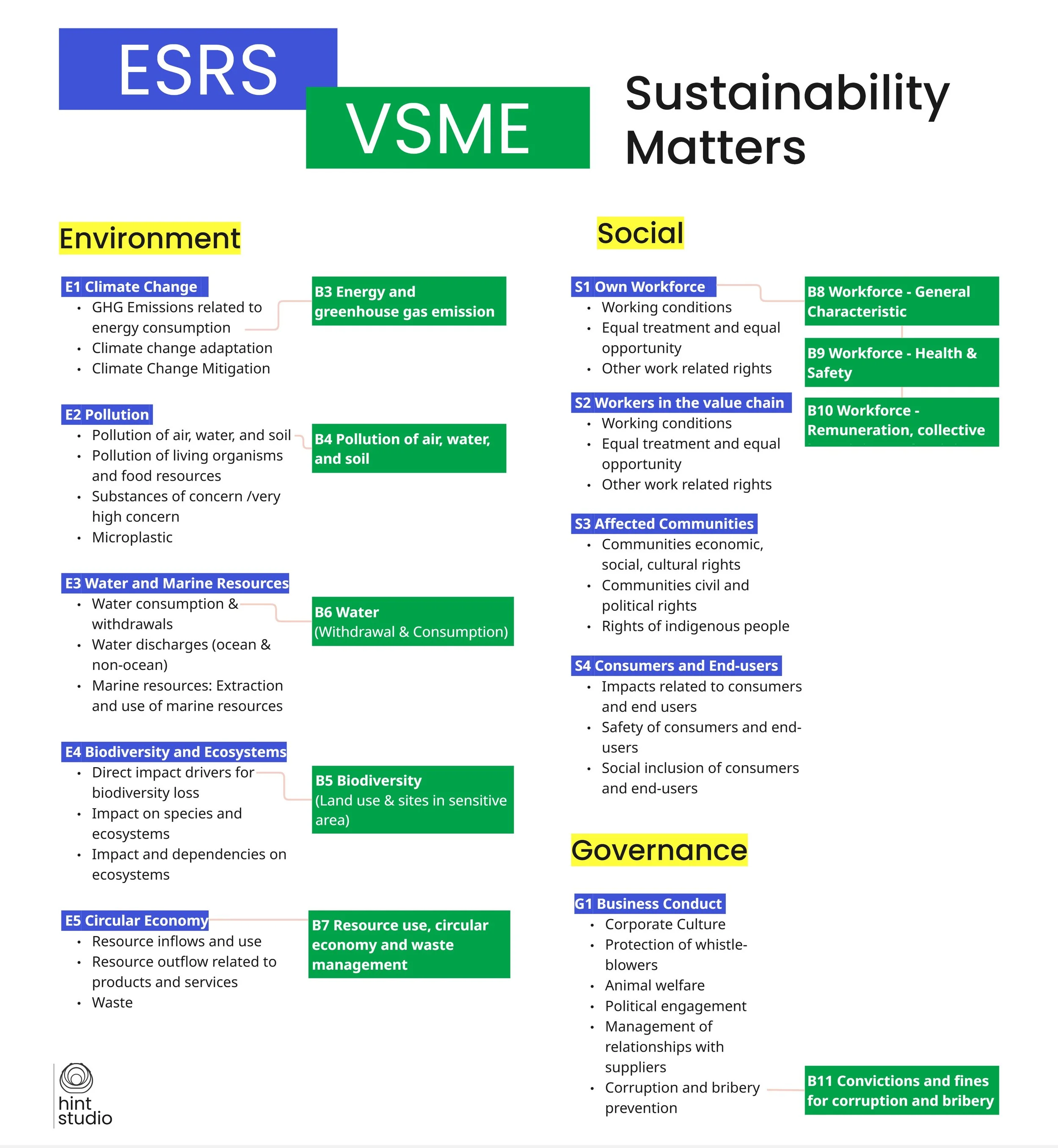

ESRS and VSME: More Connected Than They Appear

One of the least discussed — but most practically useful — aspects of the current sustainability reporting landscape is the shared foundation between the ESRS and the VSME. Both standards are built on the same underlying set of sustainability matters: defined in AR 16 of ESRS 1 (General Requirements) and Appendix B of the VSME exposure draft.

In practice, this connection is not obvious. Each standard has its own structure, and similar topics are labelled differently — giving the impression that they are entirely independent. But once you map them side by side, the relationship becomes clear: every metric in the VSME corresponds to a topical standard within the ESRS. This means that data collected through the VSME framework can serve as a foundation that is easily expanded as a company grows and potentially comes within ESRS scope in the future.

Ideally, the VSME would be designed so that its metrics transition smoothly into ESRS topical standards — a framework that scales alongside the organisation. The current design does not make this seamless, but the underlying alignment is there for companies willing to leverage it.

ESRS Topical Standard & VSME Basic Metrics

The Broader Value of the Sustainability Matters Framework

Beyond reporting, the sustainability matters framework shared by both ESRS and VSME offers a practical foundation for building sustainability strategy across the business. It provides a structured way to navigate other Green Deal regulations — for example, the Packaging and Packaging Waste Regulation (PPWR), Corporate Sustainability Due Diligence Directive (CSDDD), Digital Product Passport (DPP), and Ecodesign for Sustainable Products Regulation (ESPR) — by identifying which sustainability topics are relevant to your specific business context.

When this framework is embedded into business strategy rather than treated as a compliance exercise, reporting becomes a natural output — documentation of how the business operates — rather than a separate project layered on top. This shift in framing is significant: it moves sustainability from a burden to a business function.

Why SME Reporting Still Matters

A common objection to SME sustainability reporting is that individual small businesses have minimal environmental or social impact compared to large multinationals. It is a fair point in isolation — but it misses the aggregate picture. SMEs represent more than 99% of all businesses in Europe. Their collective footprint is enormous.

This is where the combination of the VSME and XBRL — the digital tagging system developed by EFRAG for data reported under both standards — becomes particularly valuable. XBRL enables structured, machine-readable data collection at scale. Aggregated SME data, broken down by sector or region, can offer policymakers meaningful insights for designing targeted support, funding, or incentive programmes.

Take water consumption as one example. Regional data from SMEs in areas of potential water scarcity could directly inform policy decisions, infrastructure investment, or sector-specific guidance. The value is not just in the individual data point — it is in what becomes visible when data is collected consistently and at scale.

Planning Ahead: Building Strategy From Within

Regardless of where the regulatory landscape settles, the most resilient approach is to integrate sustainability thinking into how the business operates — not treat it as a compliance obligation triggered by external requirements.

When the systems within an organisation are structured around the sustainability matters framework, reporting becomes part of a natural documentation process rather than an additional project. It captures what the business already does. The report — whether voluntary or mandatory — then becomes an output of that practice, not the driver of it.

The regulatory picture will continue to evolve. What we can do now is plan ahead, build internal capability, and remain positioned to adapt — whichever direction the regulations move.

Check our ESRS x VSME Open Board to access and review the original frameworks and relevant documents mentioned in this article.

Contact us at connect@hint-studio.com if you have issues accessing the board or any questions about our content and services.