ESRS: Simplification & the Omnibus

Snapshot from "EFRAG unveils Draft Simplified ESRS: A European Milestone for Sustainability Reporting" on 4th December 2025

Our work this year continues to focus on understanding and managing the implications of the proposed simplification of the European Sustainability Reporting Standards (ESRS).

Last December, EFRAG held an event to present their technical advice on the simplified draft of the ESRS which is currently under review by the European Commission (to learn more). This effort was part of the Commission's Omnibus package, which aims to reduce companies' burdens while maintaining the Green Deal's fundamental objective. The initiative was driven by the insights and recommendations from the Draghi report .

The Simplified ESRS Proposal

Under the current proposal, mandatory data points are reduced to approximately 61% of the original requirements, and all voluntary data points are eliminated. Thus, in this form, the proposal is leaner and easier to digest, especially for companies that are just starting their sustainable reporting journey. The voluntary data points will no longer be part of the regulations instead will be turned into 'non- mandatory guidance'. Such a guide can be interesting for mature companies that are looking to expand their sustainability efforts and opportunities.

The standard was initially developed from a scientific perspective, emphasizing evidence-based reporting and rigorous verification of claims. Such approaches—rooted in auditability, consistency, and methodological rigor—are well established within the scientific community. However, when applied in industrial contexts, these requirements raised concerns among some industry stakeholders regarding feasibility, cost, and proportionality.

The simplification reflects the ethos of focusing on what is already there rather than searching for everything according to the standard; the effort instead focuses on what can be reliably reported. Companies can also include in the report when something is unknown, or no reliable data can be obtained. Providing companies with the time and resources to make progress, and nurturing continuous internal effort to build clarity on the business and its activities in relation to sustainability.

During the December event, industry representatives highlighted that frequent changes and delays create real challenges for companies. Strategic planning and investment decisions must still be made, and the uncertainty following the Omnibus announcement in February 2025 and the waiting period for the Simplified ESRS have, for some organisations, disrupted sustainability priorities and implementation efforts.

At this stage, the technical proposals for simplifying the ESRS have been presented, and attention now turns to the forthcoming political decisions that will determine their final form.

What’s next?

In the meantime, what can companies do to plan and prepare their business when it comes to sustainable reporting? Also, a famous question we received is: With the Simplified ESRS, would the time and cost of reporting reduce significantly as well?

and…

The famous answer is 'it depends' ;)

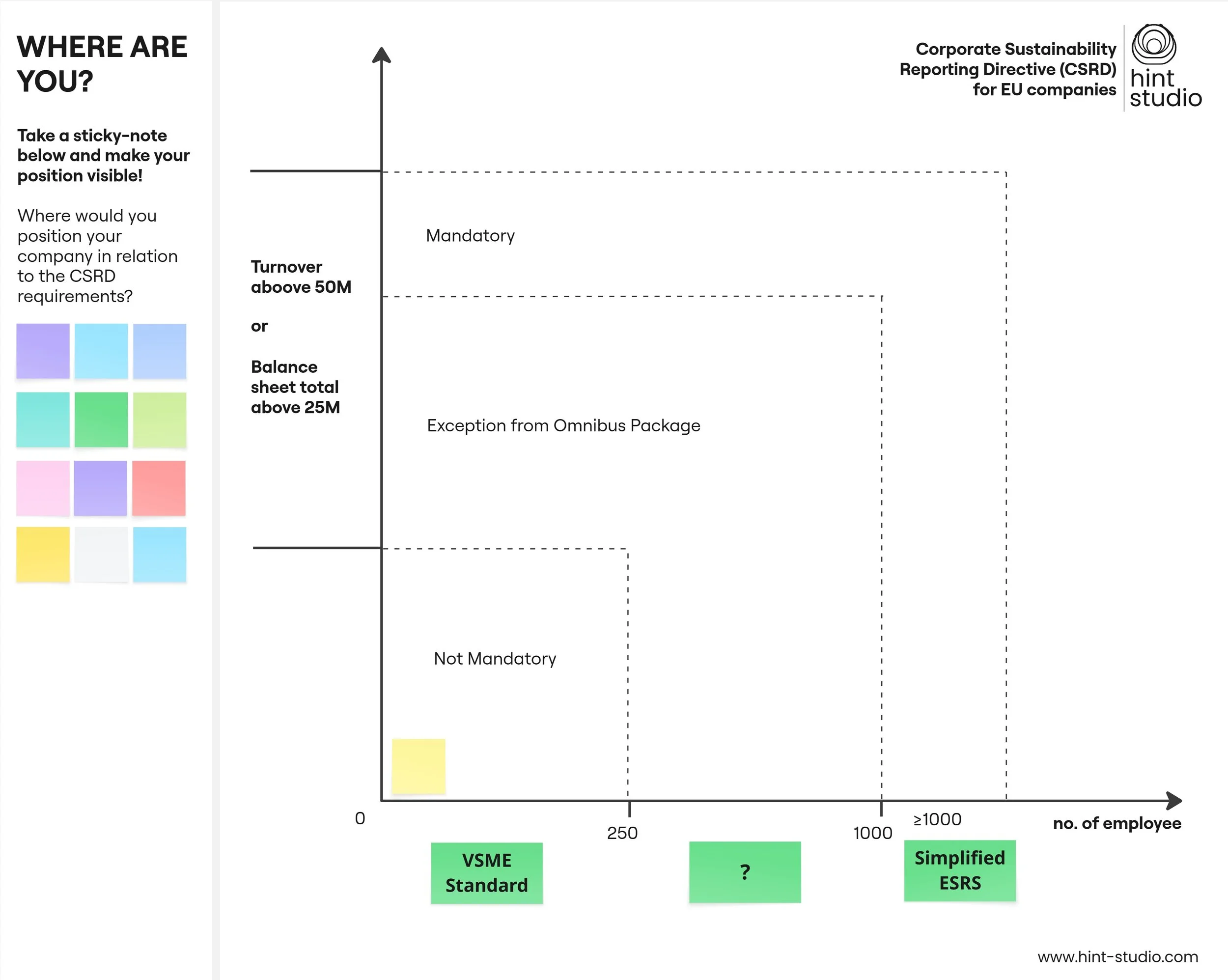

First, it's best to know where your company is positioned within the regulations. The figure below illustrates three different positions for companies based on the Omnibus package and the Simplified ESRS:

a) mandatory; b) exception from the Omnibus; c) not mandatory.

Where would you position your company in relation to the current CSRD requirements?

Where does your company currently stand in relation to the CSRD requirements?

You're also welcome to join our interactive miro board and make your position visible!

Contact us at connect@hint-studio.com if you have issues accessing the board or any questions about our content and services. I look forward to continuing this conversation in the next post.